Rising housing prices have challenged the real estate market, especially for younger generations. CNBC reported that millennials currently hold 5% of the total American wealth, making them significantly financially worse off than older generations in the past. According to Deloitte, Gen Zs and millennials regard the cost of living (e.g., housing, transport, bills, etc.) as their most significant concern.

The rise of DeFi has, however, brought with it new wealth. It is estimated that 22% of American adults own cryptocurrencies, with millennials leading the way. The more successful of these would be “Crypto Natives”- asset owners with most of their wealth in crypto assets on blockchains. One of the issues they face is diversifying their assets into the real world.

Diversifying asset portfolios with real estate

For many, real estate is one of the most stable asset classes and poses a solid barrier to entry for these “crypto natives.” Many no longer have a paycheck, receiving most of their income from DAOs or selling their assets. Most mortgage providers deem the assets too risky to offer as collateral.

“We are facing certain constraints from banks,” said Josef J, CEO and Co-founder of PWN Finance at ETHBarcelona. “Even in places like Switzerland, where crypto is quite normal now, it doesn’t really matter what you do. As long as you mention the magic word like crypto or blockchain, they won’t very likely open up a bank account for you. It’s likely they won’t want to work with you at all.”

In addition to this, he explained that there is an aspect of decision-making in play. “You have to choose. Either keep those assets for future financial system exposure or sell them. You’ll go through taxation equity to buy a property with that money, so you lose exposure to the future to buy something in the present.”

From another angle, there is a demographic of crypto natives that, although they have the wealth, want to buy real estate in markets more stable than their own.

Josip Rupena, CEO and Founder of Milo Credit, said, “Individuals are amassing wealth overseas but choosing to invest in the US because of the stability. Most of the time, they are doing it without a loan. Everybody told me it was because they didn’t want loans, but that isn’t true.”

“The system is just not designed for them. In this case, they don’t have social security numbers, they don’t have tax returns, and they don’t make income in the US. But they have something else that is interesting, which is wealth.”

Different approaches to solving the issue

PWN and Milo are working to solve these issues and better cater to the needs of crypto natives with very different approaches.

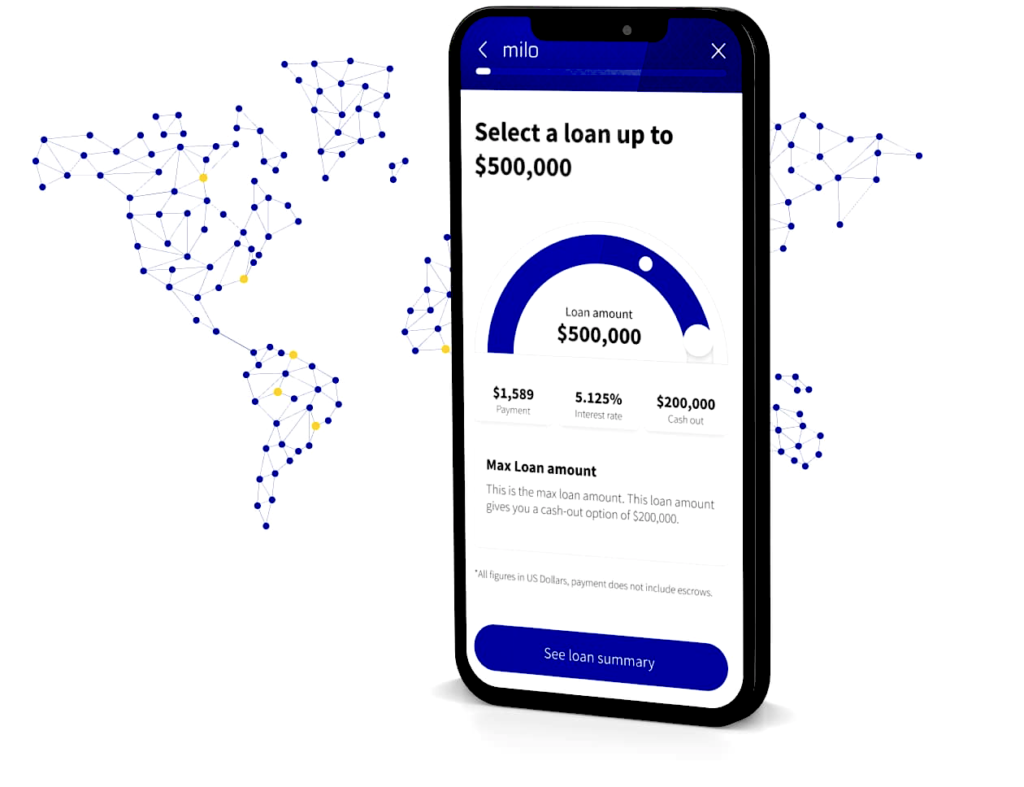

Milo was founded focusing on applicants with general wealth accumulation and released a crypto mortgage this year. They accept crypto collateral in the form of bitcoin, ethereum, and USDC for mortgages without down payments but with the value of the assets equaling the property’s value. Assets are locked within a third-party custodian.

The loan’s interest rate is adjusted according to the price of bitcoin. If the value rises after the one-year mark, borrowers can withdraw some of the assets.

“A big component of how we were thinking about this product is how do you underwrite a consumer that has assets the majority of the world don’t believe have any value,” said Rupena.

“We wanted a consumer to be able to continue to hold their bitcoin for longer periods, and we wanted them to be able to diversify, so be able to purchase real estate and not have to choose one or the other. With that, the way that we structured our transaction was that we’re going to allow a consumer to be able to buy 100% up to the value of the purchase. They wouldn’t have to bring any dollars to the table.”

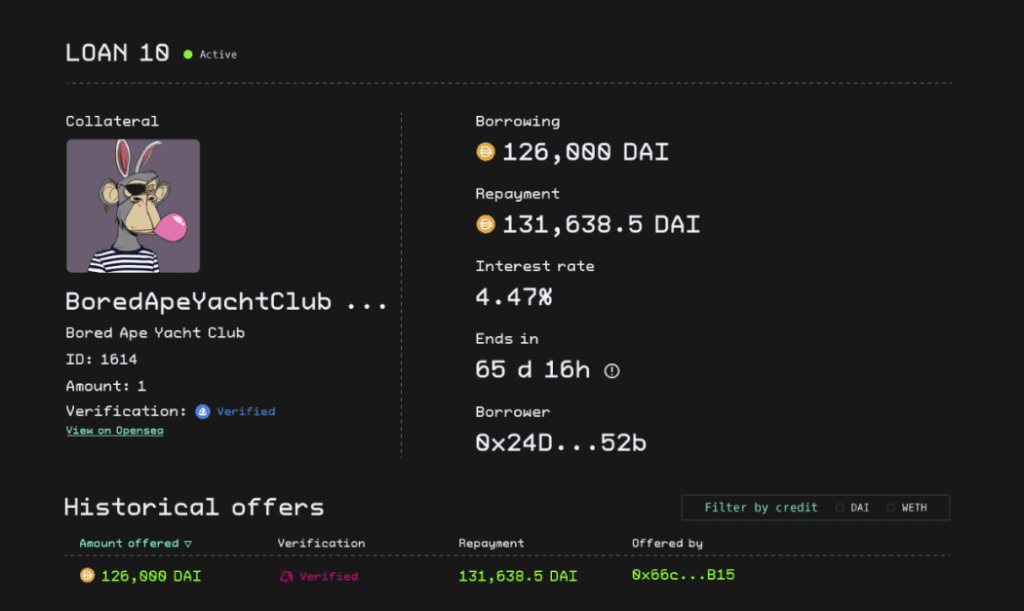

PWN works with a peer-to-peer lending model, accepting cryptocurrencies and other digital assets such as NFTs. They provide the framework for borrowers to include their assets within a smart contract, receiving fiat from lenders within a fixed term loan at a fixed interest rate.

With the use of smart contracts, the ownership of the assets remains locked within the loan until it is paid off. They are testing models where borrowers can still use assets but are locked off from withdrawing or selling them. This works to facilitate cases of game NFTs used as collateral, with the borrower still retaining rights to use the NFT to the game despite not fully paying off the loan associated.

“What we are building towards is a full-blown case where we’re setting up a protocol where the DAO will collect all of the fees and will decide the basic parameters. We’ll be getting gradual payments, enabling us to offer longer-term loans,” said Josef.

Operating within a crypto downturn

A drawback of crypto wealth, in the eyes of traditional finance, is the volatility of its value, a factor crypto mortgage issuers will also have to contend with.

PWN implements fixed terms, stating there is “no risk of liquidation before the loan expires.” The company now facilitates smaller loans, suitable for mortgage down payments rather than the whole mortgage. Fluctuations in the value of the underlying collateral aren’t seen to pose a threat as long as the loan is paid back on time.

Milo, on the other hand, offers complete mortgages, increasing the risk of default, especially in a crypto winter. However, Rupena hasn’t yet found it to be an issue. Having approached the market with that volatility, Milo has managed to weather the storm.

“How we mitigate around that volatility is rooted in our loan structure. We are requesting more digital collateral than a conventional loan, where you may have a down payment of maybe 20% or 30%, but you have no volatility. In this case, we have to offset that volatility by requiring more to withstand periods of drawdowns.”

To offset the volatility, they have implemented a margin call, whereby if the value of the cryptocurrency drops to the value of 65% of the loan amount, they will request the borrower add collateral. If the value drops to 30%, they may liquidate the assets into fiat.

“Fortunately, we’ve had no margin calls since we started originating the product despite the crypto downturn. It’s been in line with our models. Of the consumers that have gotten to levels that are closer, they decided to transfer more.”

“The individuals that take out a loan with us are watching the markets very, very closely. But ultimately, it’s having sufficient collateral protection that helps to mitigate risk.”

Related:

The post Bringing crypto natives into real estate appeared first on News.